In recent times, the Mutual Fund industry has witnessed a series of downgrades and defaults. Starting from the IL&FS, Essel, DHFL to Franklin, Birla and nippon. These downgrades or defaults can cause huge losses for investors who have parked their life-savings into these funds. Thus to protect investors from these defaults, SEBI announced the launch of the side-pocketing or segregation framework.

Many beginner to intermediate investors are unfamiliar of the concept of side-pocketing and how it can affect them, which makes it even more important for them to understand this very concept.

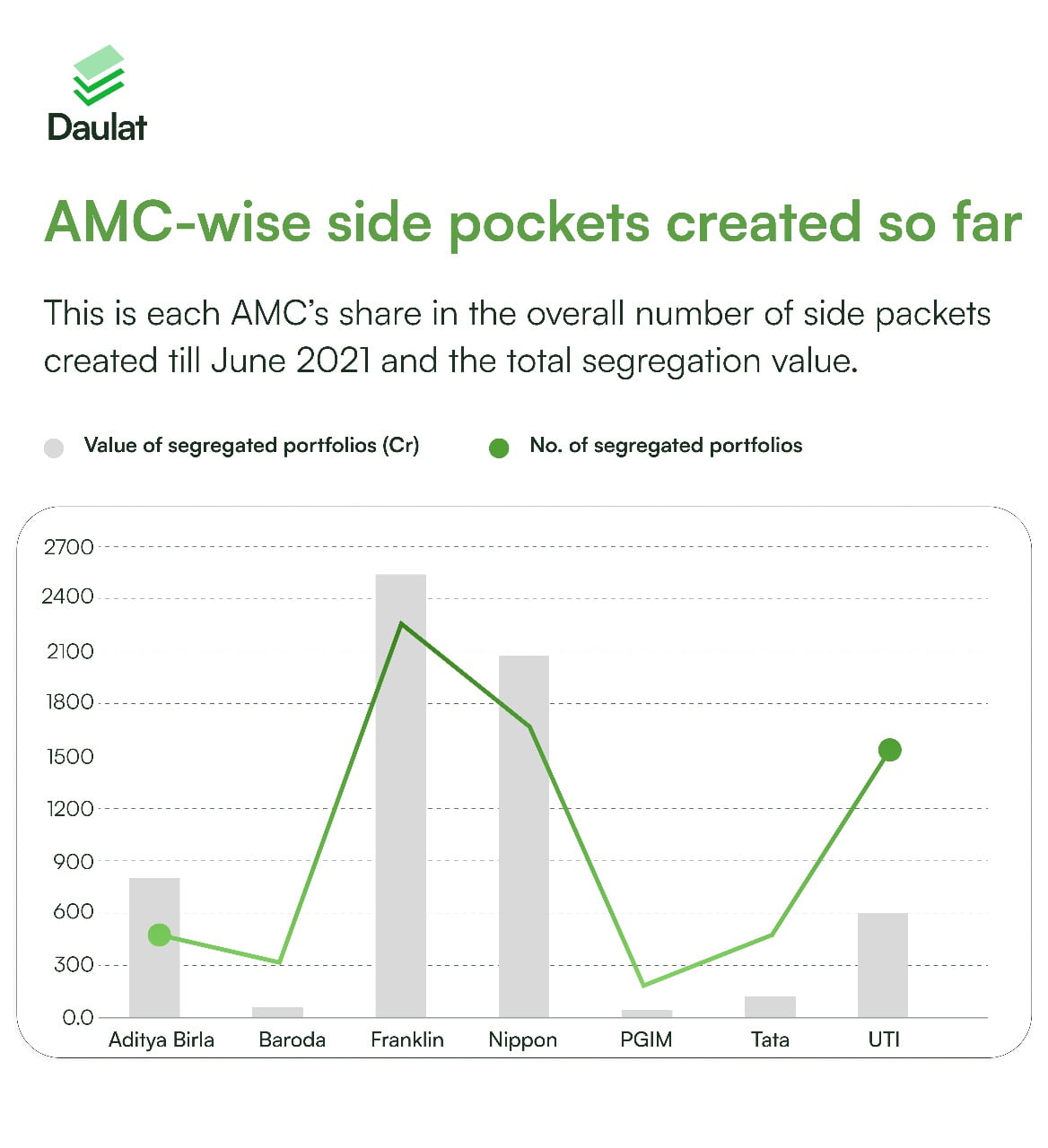

What is Side-Pocketing in Mutual Funds or Segregation of the Portfolio?

Simply put, side-pocketing is a framework that grants mutual funds the power to segregate the bad assets in a separate portfolio within their debt schemes. The Securities and Exchange Board of India (SEBI) introduced this very framework in December 2018 — primarily triggered by the IL&FS fiasco. The side pocketing framework was launched by SEBI so that the existing investor in the scheme may get the benefit whenever the money recovers. This is also to discourage the new investors from entering the scheme after the event, so as to not take undue advantages of the situation.

When does side-pocketing occur?

As per SEBI regulations, side-pocketing in mutual funds can be done only when there is an actual default of either the interest or principal amount of investment or if a debt instrument is downgraded to below investment grade or BBB rating by credit rating agencies, then the fund house has the option to create a side pocket and segregate their funds.

When side pocketing in mutual funds is done, the fund house is not sure whether the security would be realizing something later or not, but the net asset value of the fund is reduced with immediate effect.

So, in this scenario, the existing investors of the fund are allotted an equal number of shares in the segregated portfolio as held in the main portfolio and no redemption or purchase is allowed in the segregated portfolio. These shares are then listed on the stock market within 10 days and investors can sell them within a 30 day window, without any exit load/fee.

How does side-pocketing benefit the retail investor?

Once the shares of the segregated fund are listed on to the stock market and are ready to be sold, it gives full autonomy to the investor and lets them do whatever seems fit to them. Effectively, this process makes the price discovery of the bad assets a transparent procedure with investors having the freedom of either selling it at prevailing price or holding it if they expect the value to recover in future.

Can side-pocketing be misused?

When side pocketing was introduced, a good chunk of market participants felt that it could be misused by fund houses to hide their bad investment decisions. SEBI, however, has put in place checks and balances to minimize any such malpractice by the fund houses. The regulator has said that trustees or higher echelon of all fund houses will have to put in place a framework that would negatively impact the performance incentives of fund managers or chief investment officers (CIOs) or any stakeholders involved in the investment process of securities under the segregated portfolio.

So, fund managers know that any creation of such side pocket in the future would also affect their own appraisals and incentives. Further, SEBI has also said that side pocket should not be looked upon as a sign of encouraging unwanted credit risks as any misuse of this option would be considered serious and stringent action can be taken.

In Conclusion

Side-pocketing in mutual funds or Segregation of the Portfolio is a quite beneficial approach for the retail investors who lose their hard-earned money due to unwanted defaults in the debt funds. And it is quite logical that those who actually lose should only get the benefit of recovery too, and no other person should be allowed to make use of the situation as it used to happen earlier.